By Kash Reid-Bashir

Implications for Financial Services and Technology firms in the UK.

I thought it was worth looking at the effects of a British exit from the European Union (Brexit) on both the financial services and technology sectors as we enter was is likely to be a tumultuous period in the UK.

I recall being asked for some comment by a friend based in the Americas immediately after the referendum had taken place and I remember forwarding the following thoughts:

‘Those of us who are Europhiles, and I would include myself in that category, believe this is a retrograde step which is likely to see the UK suffer to a greater or lesser extent from an economic perspective over the short to medium term. Over the long term, it is possible that London’s leading European position in both the Financial Services sector and Technology sector will pass to other locations.

There is also a possibility that this result will lead to the break-up of the UK as Scotland and Northern Ireland voted to remain within the EU and as distinct territories may well eventually exit the UK.

Finally, this may well invigorate anti-EU sentiment across the continent leading to further referendums in other member countries. There is a possibility this could lead to further uncertainty and possible eventual dissolution of the EU. Although this remains a worst case scenario even from a UK perspective.’

In retrospect, I am so pleased that contagion has not occurred within Europe as no further referendums are planned, for the moment. As a result, we are likely to see a more confident stance in Europe as those who remain will arguably be more cohesive in spite of the UK exit. I am also relieved that an official Scottish Independence referendum has not been announced thus far as any further instability would not be advisable given the precarious position of the UK.

The Facts

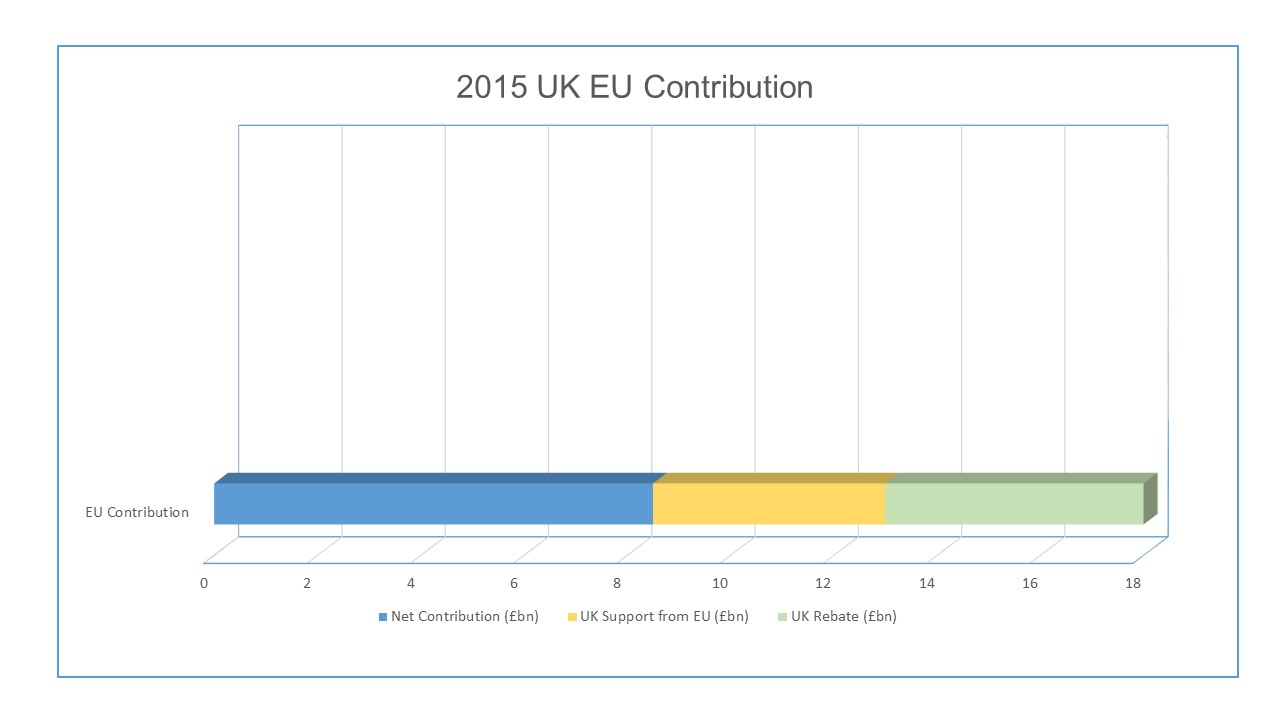

As it has become clear that a UK exit is imminent, it is worth running through the facts related to the UK economy and its economic relationship with the European Union. In particular, some clarity on the UK contribution to the EU is provided by the graphic below. Please click on the graph to gain a clearer view.

Figures relate to 2015: ‘HM Treasury, European Union Finances 2015’, Article 311 on the treaty of the functioning of the European Union.

The graph above breaks down the headline £18bn contribution into its constituent parts, with a rebate of £5bn and EU aid to the UK of £4.5bn in the form of support for agriculture and deprived areas. This leaves the high-level net contribution at around £8bn.

On more detailed examination, the net contribution made by the UK to the European Union (EU), is much lower than the £350m per week (£18.2bn per annum) advertised during the referendum campaign. According to an analysis carried out by the Times Newspaper in the UK, the actual contribution per week is £136m[i] or around 39% of the advertised figure. In other words, it is around £7bn per year if you agree with the methodology used by the Times, which calculates an annual EU net contribution figure after taking account of all monies paid back to the UK over a five-year period.

Another point of reference is provided by the treasury as we can see in the graph above, the net EU contribution for 2015 is £8bn. The Institute for Fiscal Studies in its report, Brexit and the UK’s Public Finances, uses £8bn as the net contribution for 2014.

The £8bn net contribution for 2015 provided by the treasury equates to around 0.44% of UK GDP using the figures available from the UK Office for National Statistics (2015 GDP of £1.833 trillion).

Indeed, the Institute for Fiscal Studies report[ii] indicates that an overall shift of 0.6% in national income, a close approximation for GDP, would be enough to offset the net contribution currently made by the UK. To clarify, if UK economic growth is lower than estimated pre Brexit by 0.6% in 2017, we will effectively have forgone the creation of £8bn in revenues which could have been distributed to the EU on an annual basis.

The very short term economic implications

It is now clear that the UK economy is unlikely to sustain the level of growth previously forecast for 2017, although 2016 is likely to be relatively unaffected according to forecasts at the time of writing. Estimates produced by the International Monetary Fund (IMF) for 2017 now include a 0.9% downgrade largely due to Brexit. Without extrapolating any further it is clear that any clawback of the net contribution gained through a UK exit from the European Union will be more than offset by a lack of growth in 2017 and beyond. Although this is elementary, what many observers often discount is the fact that this GDP displacement is ongoing. For example, a 1% loss in UK GDP equates to £367bn, or £18.3bn per year, in revenues using 2015 figures (undiscounted) over a 20-year period more than negating any effect of a net contribution clawback.

So it is now abundantly clear to all, if it was not during the referendum campaign, that the case for EU exit for the UK had no legitimate economic foundation.

The medium to long-term economic implications

When we start to look out further than say around three years, things become more difficult to predict. So as a note of warning all we can do here is provide some broad indications of the likely economic implications.

Over the short to medium term, it is probably fair to assume that there will be an almost certain negative impact on growth over the next four years, 2017 to 2020. A recent report by PwC[iii] predicts a 3% lower UK GDP by 2020 on a best case scenario basis, which is conservative if you examine the range of forecasts available. This scenario was based upon the successful conclusion of a Free Trade Agreement (FTA) which is likely but not a certainty. However, even if we assume that a FTA can be successfully negotiated the loss to the UK economy is significant over a period of around 20 years. A loss of 3% of GDP over a 20-year period, would equate to around £1.1 trillion, or around £55bn per year, on an undiscounted basis. So although a loss of 3% of GDP does not seem significant at first view, the absolute value forgone is significant if extrapolated over a longer period of time.

In my view, it is unlikely that any loss of GDP over the short to medium term would ever realistically be recovered. However, PwC do actually forecast that the net loss under this best-case scenario would actually narrow to around 1.2% of GDP by 2030 but this would be very difficult to verify.

What is absolutely clear is that most UK citizens are unlikely to even notice this 3% loss as there will still be significant growth over almost any period examined beyond say 2018, assuming there are no external economic shocks. Unfortunately, it is almost certain that the growth will just be more muted than would otherwise have been the case. Over the short term, there is likely to be a weaker currency leading to higher import prices which in turn are likely to lead to inflationary pressures and inevitable increases in the cost of borrowing. This would have an impact on consumer spending as disposable incomes are squeezed. Over the longer term, an increase in uncertainty and investment is likely to hinder GDP growth to some extent. A more in-depth analysis of this effect on individual sectors is provided below when examining the Financial Services and Technology Sectors.

Implications for the Financial Services and Technology Sector

With both the Financial Services[iv] sector and the Internet economy[v] contributing a significant proportion of UK GDP, 6.9% and 12.4% respectively, and growth it is worth looking at these specific sectors in a little more detail.

For both sectors, the uncertainty created by Brexit will allow other locations to displace growth which would potentially have occurred in London. An example of this is Berlin becoming an increasingly important location for technology start-ups. Berlin only recently, 2015, surpassed London by number and value of technology start-up based transactions[vi]. Staying with technology, a lack of regulatory harmonisation in privacy laws and 5G broadband standards could also hurt London from a structural perspective unless steps are taken to mitigate these effects.

As for financial services, we can expect Paris and Frankfurt to be the main European challengers to London from a geographic point of view with Euro denominated business first to come under a direct challenge. A PwC report forecasts a disproportionate sector based GVA (Gross Value Added) decline of 5.7% (base case). PwC go on to mention that the UK’s position as a global financial center could be under threat over the medium to long term based on decisions around where certain activities are based geographically.

In summary, both the Technology and Financial Services sector are likely to be challenged both from a resource perspective, with individuals increasingly targeting the most interesting opportunities, and from a geographic perspective with organisations opting to locate activities away from the UK due to market-based and regulatory issues. Finally, other challenges including issues surrounding market confidence, availability of finance and the ability to successfully innovate come under pressure as the eco system retracts resulting in fewer opportunities and potentially lower levels of productivity for incumbents and new players.

A Flawed Rationale

Assuming UK citizens were well aware that the economic case for a British exit was not positive, the only conclusion one can draw is that informed voters backing exit based their rationale on ‘taking back control’ and limiting immigration to the UK. Unfortunately, given the global nature of business and capital flows, control generally no longer rests with individual nation states as demonstrated only too clearly by events set in motion after the 2008 collapse of Lehman Brothers. If we assume that ‘taking back control’ also covers law governing the UK, one must remember that precedent set in one geography, specifically nations which share a close proximity, generally influences legislatures locally and globally so any variation in legal precedent or law created by European courts is only likely to be altered at the margins by newly created UK law and precedent. Given this is the clearly the case, the only credible rationale for exit rests on controlling immigration to the UK. Again, this case is fundamentally flawed and mainly based on fear as opposed to the economic rationale. The UK clearly benefits economically from EU migration. The PwC report mentioned above estimates that GDP growth will be 0.4% lower by 2030 purely due to lower levels of net migration to the UK. In summary, the UK will be a poorer nation both culturally and economically through rejection of the free movement of labour, one of the four fundamental freedoms of the EU.

Post-Truth Politics – The reality appeals to the worst human instincts

Shortly after electing a London Mayor, who is Asian by origin, and in turn embracing the diversity and multicultural nature of a global location, on the face of it, the UK as whole has rejected the idea of openness. The irony is palpable. Many believe we have entered a phase where fundamental truths are completely ignored in political campaigning. If we examine the Brexit campaign this certainly seems to be the case. For those of you who believe that the leave camp was guilty of conducting a campaign which was genuinely ‘dishonest’, it is worth reviewing three presentations. One given by Professor of Political Science at the LSE, Simon Hix, delivered on the 30th June 2016[vii]. The next two are by Professor of Political Science at Liverpool University, Michael Dougan, delivered on the 14th June 2016[viii] and 30th June 2016. Both individuals are respected authorities in Political Science. Simon Hix provides a review of the issues after the result has been announced and Michael Dougan reviews the issues prior to the referendum and after the result is announced. Michael Dougan’s post result review[ix] is one of the most devastating appraisals of a political campaign I have ever had the time to review and could only have gone so viral in this day and age. Professor Dougan takes each pledge made by the leave campaign and reviews it based on how truthful it seems using objective points of reference. Unfortunately, in most instances, there is absolutely no basis in fact for assertions made during the campaign. If the Trump campaign, in the US, has not left you wondering how the democratic process is fundamentally flawed, then this review certainly provides pause for thought.

A watching brief

For those from the regions, excluding Scotland and Northern Ireland, who it seems primarily voted to leave the EU on the basis of a perception that their communities were being subsumed by EU migration should actively review whether their economic situation improves on an ongoing basis. The combination of austerity and a shift in economic wealth and earnings to those at the higher end of the spectrum are not likely to subside anytime soon. However, the comfort of a collective approach to managing regional development, agriculture, and a legislative safety net for those who are most in need in our society will be removed with immediate effect. The UK’s Relative wealth and status within Europe should also be monitored actively as the direction of travel may not please the very people who voted in their millions to exit the European Union. Sadly, the opportunity to re-engage with the European project may be closed for some time as the current government is pursuing what can only be described as an accentuated, populist and rather closed vision for our country.

Conclusion

On a wide-ranging basis, the UK is arguably likely to be perceived as insular, regressive and rather less cosmopolitan in both ambition and achievement. So for all the intelligence and research on diversity being a prerequisite for industry-changing innovation, the UK has effectively taken a step backward. In my experience, once this becomes an entrenched global perception, talented individuals are likely to actively avoid seeking out the UK as a desirable place to do business, study or become a resident. This, in turn, will lead to a lack of opportunity for all as innovation in critical sectors, including technology and financial services, drive a disproportionate level of growth in the UK economy.

Kash Reid-Bashir, Founder Director, Converge Advisors and Associates

Kash Reid-Bashir, Founder Director, Converge Advisors and Associates

Converge Advisors and Associates was founded by Kash Reid-Bashir an independent, corporate financier with extensive strategy and finance experience within the media, technology and telecoms sectors. Kash has previously been part of Booz Allen Hamilton, Thomson Reuters and FTSE (a Pearson / London Stock Exchange joint venture). Kash graduated with an MBA from Cranfield School of Management.

References

[i]The Times, editorial, 18 Jun 2016

[ii] Brexit and the UK’s Public Finances, Institute for Fiscal Studies, IFS Report 116, May 2016

[iii] Leaving the EU: Implications for the UK economy, PwC, March 2016

[iv] Leaving the EU: Implications for the UK financial services sector, PwC, April 2016 (2015 Estimated UK GDP contribution from Financial Services derived using figures contained in the report)

[v] The internet economy in the G20, Boston Consulting Group, May 2015 and Press Release, The internet now contributes 10% to the UK Economy, Surpassing Manufacturing and Retail Sectors, May 2015 (The figure used above is the BCG forecast figure for 2016 UK GDP at 12.4% related to the Internet Economy)

[vi] Fortune Magazine, What Brexit means for Tech, David Meyer, June 14, 2016

[vii] After the EU Referendum: What Next for Britain and Europe?, London School of Economics and Political Science, 30 Jun 2016, Professor Simon Hix, https://www.youtube.com/watch?v=3p9hxtGltlU

[viii] Michael Dougan, Professor of Political Science, Liverpool University, on the EU Referendum, 14 Jun 2016,https://www.youtube.com/watch?v=USTypBKEd8Y

[ix] Michael Dougan, Professor of Political Science, Liverpool University, assesses UK’s position following vote to leave the EU, 30 Jun 2016, https://www.youtube.com/watch?v=0dosmKwrAbI